Between November 2021 and May 2023, the Reserve Bank (RBNZ) lifted the Official Cash Rate (OCR) from its all-time low of 0.25% to 5.50% – a level not seen since before the GFC, in 2008.

As a result, mortgage rates soared. In August 2021, the average one-year fixed rate for owner-occupiers on Canstar’s mortgage database was 2.58%. And by January 2024, it was 7.5%.

But, thankfully, peak mortgage pain has passed. Between August 2024 and last November, the RBNZ cut the OCR nine times, to 2.25%. But whereto from here?

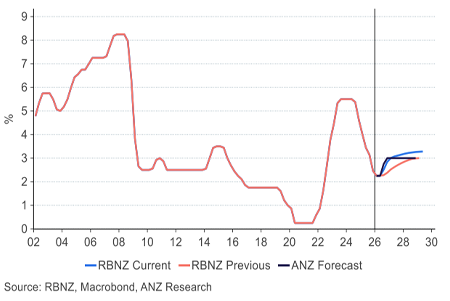

As you can see from the RBNZ’s revised projection, it seems the only way for the OCR is up:

RBNZ OCR prediction

As a result, home-loan lenders have already started to lift their longer-term rates. Since the beginning of the year, on Canstar’s database, average 1- to 5-year mortgage rates have increased by 44bps.

So given that indicators point to a higher OCR and mortgage rates, what are the major banks predicting over the coming months? Let’s take a look.

Below are synopses of the banks’ outlooks. Click on each bank’s name to jump to a more detailed overview of its predictions. And click here to see where, historically, mortgage rates have sat in relation to the OCR.

- ANZ: Predicts three more rate rises for the OCR, to 3%, by Christmas. While the one-year rate might lift slightly, before holding steady, one- and two-year rates could fall slightly from their current levels over the next 18 months.

- ASB: Expects the RBNZ will lift the OCR to 3% by the end of the year. As a result, it predicts mortgage rates are likely to increase over the next year, due to upward pressure from both local and global developments.

- BNZ: Thinks the OCR will hit 4% by May 2027, which is higher than market pricing (3.7%) and the RBNZ (3.2%) expect. If the BNZ’s forecast is correct, this is sure to lead to higher mortgage rates over the next 12 months.

- Kiwibank: Is focused on the downside risks associated with premature rate hikes, and hopes the OCR doesn’t have to lift beyond 3% until 2028. In this scenario, the pressure will come off mortgage rates over the next 12 months.

- Westpac: Expects the OCR to lift to 3% by the end of the year, and that mortgage rates will follow. Therefore, the bank thinks that mortgage rates for fixed terms between two and five years are now attractive.

Lowest Mortgage Rates for Refinancing

Looking to refinance your mortgage? The table below displays some of the one-year fixed-rate home loans on our database (some may have links to lenders’ websites) that are available for home owners looking to refinance. This table is sorted by current interest rates (lowest to highest), followed by company name (alphabetical). Products shown are principal and interest home loans available for a loan amount of $500K in Auckland. Before committing to a particular home loan product, check upfront with your lender and read the applicable loan documentation to confirm whether the terms of the loan meet your needs and repayment capacity. Use Canstar’s home loan selector to view a wider range of home loan products. Canstar may earn a fee for referrals.

Compare Lowest Home Loan Rates for Refinancing

ANZ

The ANZ thinks that there will be three hikes to the OCR in the second half of the year, in July, September and October.

However, while its forecast peak for the OCR is 3%, the bank is hedging its bets, saying that because of the uncertainty surrounding oil prices and inflation, the OCR could, ultimately, lift above 3%, but, then again, “the OCR may not even make it to 3%!”

However, on the back of its 3% prediction, it sees mortgage rates remaining steady over the next 18 months:

| Rate | June 2026 | Sept 2026 | Dec 2026 | March 2027 | June 2027 | Sept 2027 | Dec 2027 |

| Floating | 5.80% | 6.50% | 6.80% | 6.80% | 6.80% | 6.80% | 6.80% |

| 1-Year | 4.80% | 5.00% | 5.00% | 5.00% | 5.00% | 5.00% | 5.00% |

| 2-Years | 5.30% | 5.30% | 5.10% | 5.00% | 5.00% | 5.00% | 5.00% |

| 3-Years | 5.50% | 5.40% | 5.30% | 5.10% | 5.10% | 5.10% | 5.10% |

| 5-Years | 5.90% | 5.90% | 5.80% | 5.80% | 5.80% | 5.80% | 5.80% |

So when it comes to fixing, ANZ says that one- to two-year fixed rates are the current sweet spot, because they offer a good balance of cost and certainty.

ANZ OCR Forecast

![]()

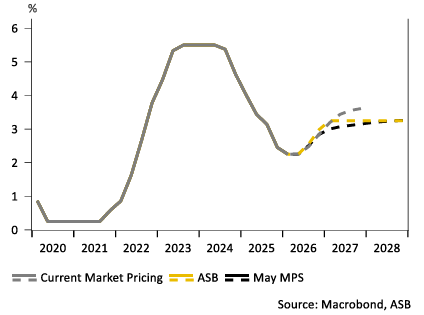

ASB

ASB economists expect the RBNZ will lift the OCR back to 3% by the end of the year. But while ASB agrees with the RBNZ that the OCR’s endpoint needs to be 3.25%, it disagrees with the speed of the increases, and thinks it needs to hit that level early, rather than later, next year.

As a result, ASB predicts that all mortgage rates are likely to increase over the next year, due to upward pressure from both local and global developments.

ASB OCR Forecast

Searching for the Cheapest Personal Loan?

If you’re looking for the cheapest personal loan, Canstar’s personal loan comparison tables can help. The table below displays the sponsored unsecured personal loan products available on Canstar’s database for a three-year loan of $10,000 in Auckland, with links to lenders’ websites. Use Canstar’s personal loan comparison selector to view a wider range of products on Canstar’s database. Canstar may earn a fee for referrals.

![]()

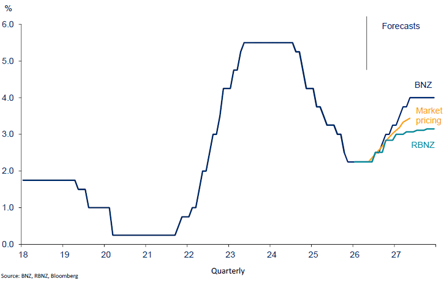

BNZ

BNZ says that the RBNZ is clear about its intention of lifting the OCR to a more neutral level, from its current stimulatory stance.

It notes that mortgage borrowers, as well as the markets, have already build these increases into their expectations.

As you can see from the chart below, BNZ thinks the OCR will hit 4% by May 2027, which is higher than market pricing (3.7%) and the RBNZ (3.2%) expect.

If the BNZ’s forecast is correct, this is sure to lead to higher mortgage rates over the next 12 months.

BNZ OCR Forecast

![]()

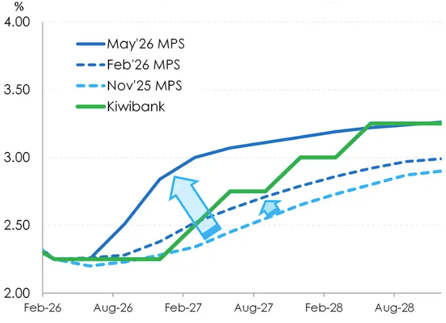

Kiwibank

Kiwibank’s economists expect the RBNZ to start hiking the OCR in July, and say that interest rates have already risen in anticipation.

However, Kiwibank is focused on the downside risks associated with premature rate hikes. And although it says the market is anticipating a swift move up past 3.5% in 2027, Kiwibank hopes the OCR doesn’t have to lift beyond 3% until 2028.

In this scenario, the pressure will come off mortgage rates, and homeowners, over the next 12 months.

Kiwibank OCR Forecast

![]()

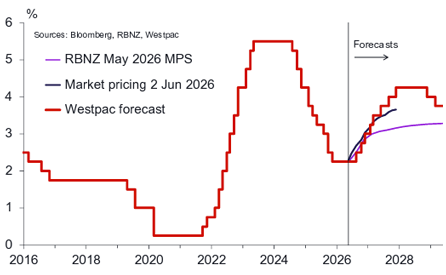

Westpac

Westpac expects 25bp rate hikes to the OCR in September, October and December, but notes that financial markets have already priced in the first rate rise in July.

And as the OCR lifts, Westpac thinks mortgage rates will follow. Therefore, the bank thinks that mortgage rates for fixed-terms between two and five years are now attractive, as they insulate borrowers from trending higher rates over the next couple of years.

Westpac OCR Forecast

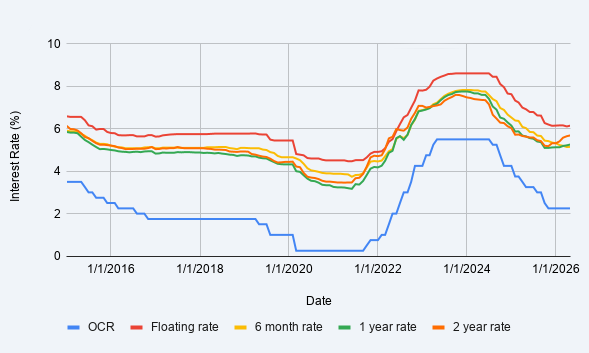

Mortgage Rates vs OCR

Looking at current predictions, over the next six months the OCR should rise to around 3%. So on such a forecast, where can we expect interest rates to settle?

The last time the OCR sat around 3%, was 10 years ago, and then the banks’ carded shorter-term rates were just over 5%, which is exactly where they’re sitting now. And as you can see below, even though the OCR did subsequently drop to below 2% in the years leading up to the pandemic, mortgage rates remained pretty static.

Although it’s worth pointing out that a bank’s advertised carded rate is different from its special rate. This means, if you’ve a 20%-plus deposit and a good credit history, you’re very likely to qualify for a better deal.

OCR vs Mortgage Rates 2015-2026

Compare Home Loan Rates with Canstar

About the author of this page

In his role at Canstar, he has been a regular commentator in the NZ media, including on the Driven, Stuff and One Roof websites, the NZ Herald, Radio NZ, and Newstalk ZB.

Away from Canstar, Bruce creates puzzles for magazines and newspapers, including Woman’s Day and New Idea. He is also the co-author of the murder-mystery book 5 Minute Murder.

Share this article