Many homeowners’ mortgages are rolling over this year, and most will face much higher rates. But there are ways to save on your mortgage repayments. Squirrel’s John Bolton has some expert advice on how to refinance your mortgage and save.

In a nutshell:

- Lots of us are due for a fixed rate rollover this year – and with rates currently at around 6.50%, that’s going to create big financial pressure for Kiwi households

- These highs are only temporary, and beyond the end of the year it’s likely that interest rates will settle back around 5%

- So it can help to think about higher mortgage costs as being made up of two parts: long-term and short-term

- Banks have really great cashback offers on refinancing deals, which could help offset a significant portion of increased costs

![]()

A lot of Kiwi are heading towards fixed-rate rollovers this year, which will see us coming off rates of around 3% to roughly 6.5%.

If you’ve got a million-dollar mortgage, the transition is going to set you back about an extra $2000 per month, or $24,000 a year. Not a lot of us have that sort of spare change floating around. So then the question becomes: How do you fill the gap?

As you’re answering this question, it can help to think about the increase to your mortgage costs as, essentially, being broken down into two parts.

Part of the increase in mortgage costs is here to stay

Interest rates just aren’t going to drop back to those lows of 2.7% to 3.5% any time soon.

But once we’re through the current period of higher rates, it’s pretty reasonable to expect that mortgage rates will come back and stabilise somewhere around 5%.

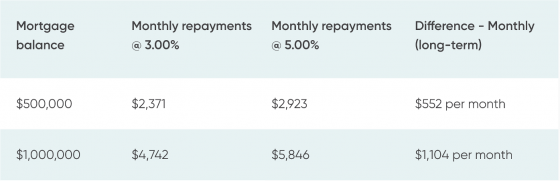

So, it’s the gap between your current rate and this “sustainable” rate of around 5% that you’ll need to make up in the long term.

You can run the numbers through a mortgage calculator to work out exactly what that looks like for your situation. But here are a couple of examples based on mortgages of $500,000 and $1,000,000.

This part of the increase you probably need to be working to cover through sustainable changes to your budget and lifestyle, to cut back on expenses. And I’ve written a separate blog article with some tips to think about as you’re going through that process.

The rest of the increase will only apply while we’re in the current period of higher rates

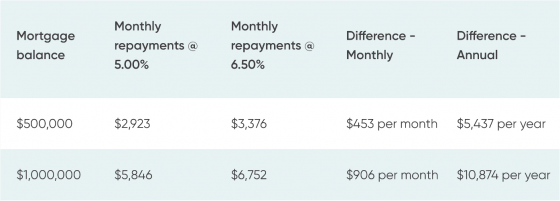

Anything over and above the 5% mark in terms of interest rates is an added cost that you should only need to grapple with relatively short term (12 months or so), until interest rates start to come down again.

(This is one reason why I’d recommend only fixing short-term in this environment – and I’ve just written a separate article talking about another very good reason, break fees.)

Here’s how the numbers work out for those same two examples.

The short-term increase works out to be roughly 40% of the overall increase in mortgage expenses that you’ll be facing into, if you’re rolling off fixed rates this year.

One really clever way to make up the short-term cost is by refinancing your mortgage and getting a cashback

There are a few different ways to go about generating the extra cash, of course – you could tap into savings or sell stuff you no longer need on Trade Me.

At the moment, though, a number of the banks are offering cashbacks of up to 1% when you refinance your mortgage – which (depending on the size of your loan, and the bank) could mean anywhere from an extra $3000 to $25,000 in your pocket.

It’s essentially free money, and it’s all non-taxable.

Going back to those same examples we were looking at before, you’ll see that the cashback essentially covers the short-term difference – or that extra you’ll have to pay over the next 12 months or so, just while rates are as high as they are.

→ Related article: Best First Home Buyer Home Loans

Refinancing also gives you the chance to restructure your finances, and your mortgage, to save costs in other ways

Refinancing gives you the chance to restructure your mortgage – which could be as simple as extending the term of your loan, or maybe popping some of it on revolving credit if you’ve got some savings already.

It also gives you the chance to consolidate really expensive consumer finance debt, or other high-interest debts, back into your mortgage, to save money on interest.

A number of the banks have also introduced green loans, where they’ll lend you up to $80,000 at 1% for three years as a home loan top-up. You can use the loan to do things like buy a hybrid or electric car or install solar panels on your property – changes which could save you money on things like electricity and petrol.

If you’re thinking about making these purchases anyway, green loans can be a great way to do it when you refinance.

→ Related article: Sustainable Home Loans NZ: What’s on Offer

![]()

What else do you need to know about refinancing if you want to get the cashback offer?

1. You’ll need to switch banks

You can’t get a cashback just by refinancing with your existing bank, unfortunately.

So, you’ll have to submit a new loan application, with the full plethora of paperwork, and pass servicing calculations (which is a bit tougher at the moment). It’s a bit of a pain in the butt, but it’s all relatively straightforward – and arguably well worth it.

It’s worth noting that KiwiBank offers a free refinance service, while other banks require the use of a solicitor. That’ll usually set you back about $1000 or so. However, Squirrel is Kiwibank’s biggest broker in New Zealand and can help with a refinance.

2. You’ll need to have been with your current bank for at least four years

If you haven’t had your mortgage with your current bank for a period of at least four years, you risk getting a clawback on your previous cash advance. If you’re not sure whether this applies to you, I’d suggest chatting with an advisor.

3. Refinancing only really makes sense if your whole loan is due to roll over

If part of your loan is still locked in at a really good rate for a while yet, refinancing won’t make much sense until that loan matures – otherwise, you’ll lose the interest rate benefit on the loan you’re breaking.

And when you’re coming off really low rates in this environment, that’s a significant benefit you’d be throwing out the window.

John Bolton founded Squirrel in 2008. He is a former General Manager at ANZ, where he was responsible for the bank’s $60bn of retail lending and deposits. He has 10 years of senior banking experience behind him in financial markets, treasury, finance, and strategy, and is a director of Financial Advice New Zealand, the industry body for financial advisers. Check out Squirrel’s website for how Squirrel helps first home buyers, here.

John Bolton founded Squirrel in 2008. He is a former General Manager at ANZ, where he was responsible for the bank’s $60bn of retail lending and deposits. He has 10 years of senior banking experience behind him in financial markets, treasury, finance, and strategy, and is a director of Financial Advice New Zealand, the industry body for financial advisers. Check out Squirrel’s website for how Squirrel helps first home buyers, here.

Enjoy reading this article?

You can like us on Facebook and get social, or sign up to receive more news like this straight to your inbox.

By subscribing you agree to the Canstar Privacy Policy

Share this article